College Costs

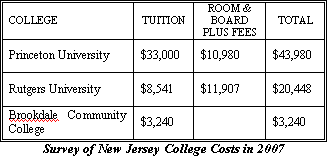

College tuition has always been expensive and continues to rise at a higher rate than general inflation. On average, tuitions in 2007 increased over 6.6% at public institutions, 6.3% at private, and 4.2% at 2-year schools. A survey of the costs of local New Jersey schools, in the table below, shows the current formidable challenge of paying for college. It is unlikely that college tuition inflation rate will decrease in the future years, as there is no incentive for colleges to do so, as more and more people attend universities each year.

Investing for College

To combat the college inflation rate, a more aggressive approach is needed than simply socking away money for 18 years in a savings account or using low-yielding EE bonds. To at least keep up with inflation, a college fund needs to average a greater that 6% return. That can only be done by having exposures to equities, which although more volatile than savings bonds, have a history of providing an average annual return of over 9% over the last 15 years. Luckily, college for Jack is 18 years away and the long time horizon allows for a more aggressive approach, as time can be used to smooth out the ups and downs of the stock market.

Savings Bonds vs. 529 Plan

People have felt safe buying savings bonds because they are guaranteed to never lose money and have a face value double of the invested principle. However, the current savings bonds are also guaranteed to not keep up with inflation. EE bonds purchased today have an interest rate of 1.4% and a maturity date of 2028. In addition, the interest is not exempt from Federal income tax. On the other hand, the 529 plan allows one to invest in a number of diversified mutual funds, tax free (not tax deferred like 401(k) or IRAs), that can provide a much greater, although more volatile, return. They benefit from the tax free growth, as well as, tax free use when used for college expenses. In addition, the fund holdings can be very conservative in Government bond funds or more aggressive in all equities, such as a small cap fund, and shifted over time from aggressive to conservative funds very simply online. These are the primary reasons we chose to open a 529 Plan, which are offered separately by every state.

Our 529 Plan

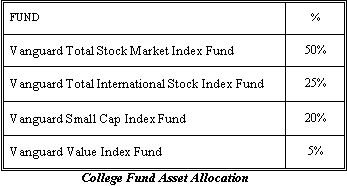

New Jersey’s 529 Plan does not provide any significant incentives for residents, so we chose our plan based on finding the one with the lowest fees and best fund options. We opened with the state of the Nevada, which is administered by Vanguard, who is known for having low cost index funds in a large number of areas. They offer a total of 22 funds in many areas in the Nevada plan. The stock market has been very volatile the past few years, with small gains seen last year and significant losses this year. This coincidentally provides a good time to start our college fund, and since it has an eighteen year horizon, we can utilize the equity funds to provide a higher return. Jack’s College fund was established with an asset allocation as follows:

- Vanguard Total Stock Market Index Fund – This mirrors the complete US stock market including the large, small, and mid caps and provides the core holdings for the college fund. The US total stock market has seen about a 11% drop this year (as measured by the Wilshire 5000), but we expect the broad stock market to recover and provide respectable results over the next eighteen years around its historical average of 6-8%

- Vanguard Total International Stock Index Fund – This is a fund of funds that includes three international funds, the European Stock Index Fund, Pacific Stock Index Fund, and Emerging Markets Stock Index Fund and provides a very diversified international weighting. Much of the growth is expected to come in the emerging and Asian markets over the next few years and provides a good uncorrelated return to the US stock market.

- Vanguard Small Cap Index Fund - This index fund follows the small cap market and provides a heavier weighting of the faster growing small cap segment of the US stock market. This boosts the small cap representation already present in the Total Stock Market Index Fund.

- Vanguard Value Index Fund – This index fund follows value stocks in the US stock market, which includes those stocks whose are considered undervalued and have great potential for growth. Including this fund provides a small additional weighting to value stock.

Our asset allocation for 2008 is shown in the table below:

No bond funds were used in the allocation for two reasons. First, with eighteen years until funds will likely start to be drawn, there is no need to be conservative now, especially as college cost are increasing at over 6% and Treasury rates are low at 3%. Second, interest rates are expected to rise over the next few years in response to the low rates we have now, and expected increase in inflation. If interest rates do go up, it would follow that bond funds will see a drop in net asset value as their yields increase. If and when that happens it may be appropriate to buy into those funds to capture some of the increase yield.

No bond funds were used in the allocation for two reasons. First, with eighteen years until funds will likely start to be drawn, there is no need to be conservative now, especially as college cost are increasing at over 6% and Treasury rates are low at 3%. Second, interest rates are expected to rise over the next few years in response to the low rates we have now, and expected increase in inflation. If interest rates do go up, it would follow that bond funds will see a drop in net asset value as their yields increase. If and when that happens it may be appropriate to buy into those funds to capture some of the increase yield.

Earn making loans

Earn making loans $25 Bonus for opening an ING savings account!

$25 Bonus for opening an ING savings account!