The Democrats made a clean sweep in elections and control the House, Senate, and Presidency. Now there are no checks and balances on what legislation they can pass. Already, there is talk of giving a way another stimulus package, bailing out the American auto manufacturers, and confiscating 401k accounts for a Government run pension-like program.

Now my worst fears of a socialist country are coming true. Clearly Obama won the election mostly due to the hate of the Bush administration, rather than his plans for the future. We know the Democrat elites have a love for Europe, but let's not turn this country into another France, where the Government protects everyone's jobs and ends up stifling innovation and economic growth. Nancy Pelosi and Harry Reid are calling for a loan package be issued to GM, Ford, and Chrysler to keep them in business. We can't start bailing out every industry. We need to allow them to sink or swim on their own. We have to allow the car companies to fix there own problems, by consolidating, reducing costs, and focusing their products to what the market wants.

Notice how the foreign car makers (who employ thousands of Americans) are having an off year, but are still making a profit. This is because they make a product that people want and can manufacture it at a low enough cost to be competitive. And they don't do this by having low paid workers in Japan or China. Toyata, Nissan, and Honda, have plants in Texas, Mississippi, and Alabama where they make cars for the US market. However, they don't have a history of bad deals and promises with the United Autoworkers (UAW).

The US companies have too many product lines, many that are unprofitable, and too many longterm pension and healthcare costs that are killing their bottomline. I heard Larry Kudlow say today that basically the US auto industry is a healthcare company that makes cars on the side. It may require that Ford, GM, and Chrysler file for bankruptcy, scale down operations, and emerge as a leaner, smaller, but profitable company. Likewise, the UAW may have to negotiate contracts that don't kill their own industry. If the Government bails them out, it will only be a temporary patch, that will re-occur over and over again.

Some may argue that if the banks were bailed out then why not a large industry like the auto industry. First, a strong banking and credit system is needed for any and all businesses to function and has world wide implications. No other industry has this far reaching effects. Second, there are alternatives and profitable car manufacturers, so if some were to disappear, it would not create all to fail, but rather strengthen the other businesses.

The airline industries have been going through a similar problem for years, it has caused consolidation, some to file bankruptcy, and new profitable competition to step up. Loaning money to a company like GM is not going to help them, as their problems are not a temporary shortfall of cash, but rather a fundamental business operations problem that won't go away without major changes to the business.

Now my worst fears of a socialist country are coming true. Clearly Obama won the election mostly due to the hate of the Bush administration, rather than his plans for the future. We know the Democrat elites have a love for Europe, but let's not turn this country into another France, where the Government protects everyone's jobs and ends up stifling innovation and economic growth. Nancy Pelosi and Harry Reid are calling for a loan package be issued to GM, Ford, and Chrysler to keep them in business. We can't start bailing out every industry. We need to allow them to sink or swim on their own. We have to allow the car companies to fix there own problems, by consolidating, reducing costs, and focusing their products to what the market wants.

Notice how the foreign car makers (who employ thousands of Americans) are having an off year, but are still making a profit. This is because they make a product that people want and can manufacture it at a low enough cost to be competitive. And they don't do this by having low paid workers in Japan or China. Toyata, Nissan, and Honda, have plants in Texas, Mississippi, and Alabama where they make cars for the US market. However, they don't have a history of bad deals and promises with the United Autoworkers (UAW).

The US companies have too many product lines, many that are unprofitable, and too many longterm pension and healthcare costs that are killing their bottomline. I heard Larry Kudlow say today that basically the US auto industry is a healthcare company that makes cars on the side. It may require that Ford, GM, and Chrysler file for bankruptcy, scale down operations, and emerge as a leaner, smaller, but profitable company. Likewise, the UAW may have to negotiate contracts that don't kill their own industry. If the Government bails them out, it will only be a temporary patch, that will re-occur over and over again.

Some may argue that if the banks were bailed out then why not a large industry like the auto industry. First, a strong banking and credit system is needed for any and all businesses to function and has world wide implications. No other industry has this far reaching effects. Second, there are alternatives and profitable car manufacturers, so if some were to disappear, it would not create all to fail, but rather strengthen the other businesses.

The airline industries have been going through a similar problem for years, it has caused consolidation, some to file bankruptcy, and new profitable competition to step up. Loaning money to a company like GM is not going to help them, as their problems are not a temporary shortfall of cash, but rather a fundamental business operations problem that won't go away without major changes to the business.

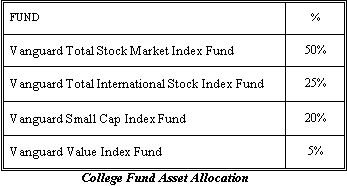

No bond funds were used in the allocation for two reasons. First, with eighteen years until funds will likely start to be drawn, there is no need to be conservative now, especially as college cost are increasing at over 6% and Treasury rates are low at 3%. Second, interest rates are expected to rise over the next few years in response to the low rates we have now, and expected increase in inflation. If interest rates do go up, it would follow that bond funds will see a drop in net asset value as their yields increase. If and when that happens it may be appropriate to buy into those funds to capture some of the increase yield.

No bond funds were used in the allocation for two reasons. First, with eighteen years until funds will likely start to be drawn, there is no need to be conservative now, especially as college cost are increasing at over 6% and Treasury rates are low at 3%. Second, interest rates are expected to rise over the next few years in response to the low rates we have now, and expected increase in inflation. If interest rates do go up, it would follow that bond funds will see a drop in net asset value as their yields increase. If and when that happens it may be appropriate to buy into those funds to capture some of the increase yield.

Earn making loans

Earn making loans $25 Bonus for opening an ING savings account!

$25 Bonus for opening an ING savings account!