I have been involved with peer to peer lending site Prosper for almost a year and a half. I decided to try it out as further diversification of my portfolio and because I thought the idea was interesting. For those who don't know, Prosper allows peer to peer loans to be made. Basically borrowers apply for a loan, and many lenders bid on the interest rate with a small piece of the loan. For the lenders, the rates are higher than you could get with a CD or money market, but for the borrowers lower than most credit card rates, usually in the range of 7-25%. However, with the higher interest rates come the risk of default. Typically, a lender would own many loans in the range of $25-$50 spread across a diverse set of credit ratings.

Not surprisingly, this interest rate mostly attracts borrowers who couldn't get a home equity or lower interest loan, so you know immediately these are rather risky loans. Doing a quick look at the lendingstats.com you can find a lot of statistics on current lenders. The average return on investment (ROI) for lenders with loans of >6 months is shown in the graph below:

I started with a pretty diversified investment of $3,187. Over the last year and half, I 've seen two loans default, two get paid off early, and the rest are current.

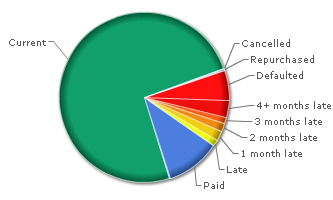

One problem with Prosper is I can’t really trust the ratings and there is a very high default rate. Virtually everyone has experienced at least one default who has loaned any sizable amount of money. The current Prosper history of all loans is shown below.

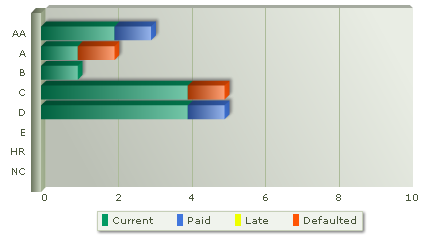

Note that 10.2% of all loans are currently 3+ months late or defaulted. Typically 3+ month late loans don't become current. Then the loans that are in really good shape, end up paying off their loan early. So you don’t make much interest off of the good loans, and you are stuck with a number of risky loans that may default. Just one or two defaults can seriously eat into your profits for the year. Last year I had about $2900 invested and ended up with net profits of $19, while my current ROI is estimated to be 7.18% for the life of the loan. Plenty of A rated loans default as well. See from my loan breakdown below that I had a diversified collection. An A and C rated loan defaulted, while a AA and D loan were paid early.

Finally, perhaps the biggest problem is there is no liquidity. There currently is no secondary market, so your money is tied up until the loan is paid off in a maximum of three years. I would consider investing on a continuous basis if I was able to pull it out when I needed. Here are a few things I've learned and suggest:

- Don't setup any automated investing through Prosper, you can use filters, but in the end you need to do a little investigating before pulling the trigger,

- Don't invest in any businesses: Most businesses go bankrupt and there is very little damage to the individual's credit (or motivation to pay off the loan) if they had it setup as an LLC.,

- Fund only smaller loans, <$3,000, as there is less chance of them falling behind.

Earn making loans

Earn making loans $25 Bonus for opening an ING savings account!

$25 Bonus for opening an ING savings account!